Having embarked on their Circular Economy journey, organisations often reach a point where the ups and downs of their activity, and the shifting priorities that might go along with them, eventually take over the initial positive momentum. It becomes difficult to keep plans on track for a prolonged period and the lack of progress may cause frustrations, if not start a demotivating spiral. This is certainly a time when senior leadership commitment and backing are essential, but their words alone may sometimes not be enough to effect real change today… sound familiar?

The reality is that most of your co-workers would easily “buy into” the destination on offer. Who does not wish for a sustainable business and a more liveable environment for their families and communities? One of the challenges you are facing is that the practical aspects of the journey to get there – often revolving around carbon accounting – involve a whole new language that is as alien as it is unappealing. You might therefore be tempted to “teach them” but I’d like to suggest an alternative approach: translating it into a language they all speak already, i.e. currency! Think about it. Do you know what a ton of carbon looks like? I thought not, but I would imagine you would have no trouble visualising a USD or EUR 10 note…

Not so surprisingly, one thing the organisations leading the way in decarbonisation, especially supply chain decarbonisation, have typically in common is an Internal Carbon Pricing mechanism or ICP. Let’s explore why you may want to consider it, how you could implement it, and yes, how much it may cost!

Why put a price on Carbon?

As alluded to in the introduction, one of the key reasons you may want to consider an Internal Carbon Pricing (ICP) is workforce engagement. This is not just the result of speaking a common language. Giving carbon a price means that what may have been an “additional target” or at times a “conflicting target” becomes a “combined target” measured using the same unit. With it, you are empowering your colleagues to make business decisions that are aligned with your sustainability objectives, as opposed to making a choice between business and sustainability. This can apply to every decision in your organisation, from strategy to investment, business case, cost optimisation or purchasing. It is also relatively easy to integrate within your existing processes from annual budgets to personal incentives, and an effective way to drive the desired behaviour.

And while the above in itself will dramatically help drive change, control its pace and articulate it to investors and other stakeholders, it will also get your organisation prepared for upcoming Carbon Tax systems, an external risk that should be on anyone’s radar. The timing of their implementation will vary depending on the jurisdiction, sector of activity and possibly company size, but one thing is certain, legislators want to see change and these mechanisms will soon become a reality. The EU Emissions Trading System (ETS) which will interact with the Carbon Border Adjustment Mechanism (CBAM) are less than four years away and will impact energy, shipping, and transportation among others. California is leading the way States-side with what is known as the California Carbon Allowance program or “cap and trade” program, and China may not be far behind in implementing their own Carbon tax…

Benefits of implementing ICP

- A common “language” to help articulate, raise awareness and understanding of circular strategy objectives with all stakeholders

- Higher staff engagement with the circular strategy

- Better alignment of objectives and more cohesive decision making

- Relatively simple integration with existing management processes

- Higher likelihood of success in circular change and faster results (incl. carbon footprint reduction)

- Preparedness and de-risking against upcoming Carbon Tax

How to implement ICP?

There are typically two ways to implement ICP: Establish a “theoretical” price – known as shadow pricing – or establish an internal trading system where “real money” is being transferred.

Shadow pricing appears to be the most common in the corporate world today, and while not as compelling as an internal trading system, happens to be very effective, still. The concept is quite simple: the cost of carbon is simply added to the actual cost of doing business in all the key processes, directly impacting their outcome as a result – as demonstrated in the hypothetical scenario below.

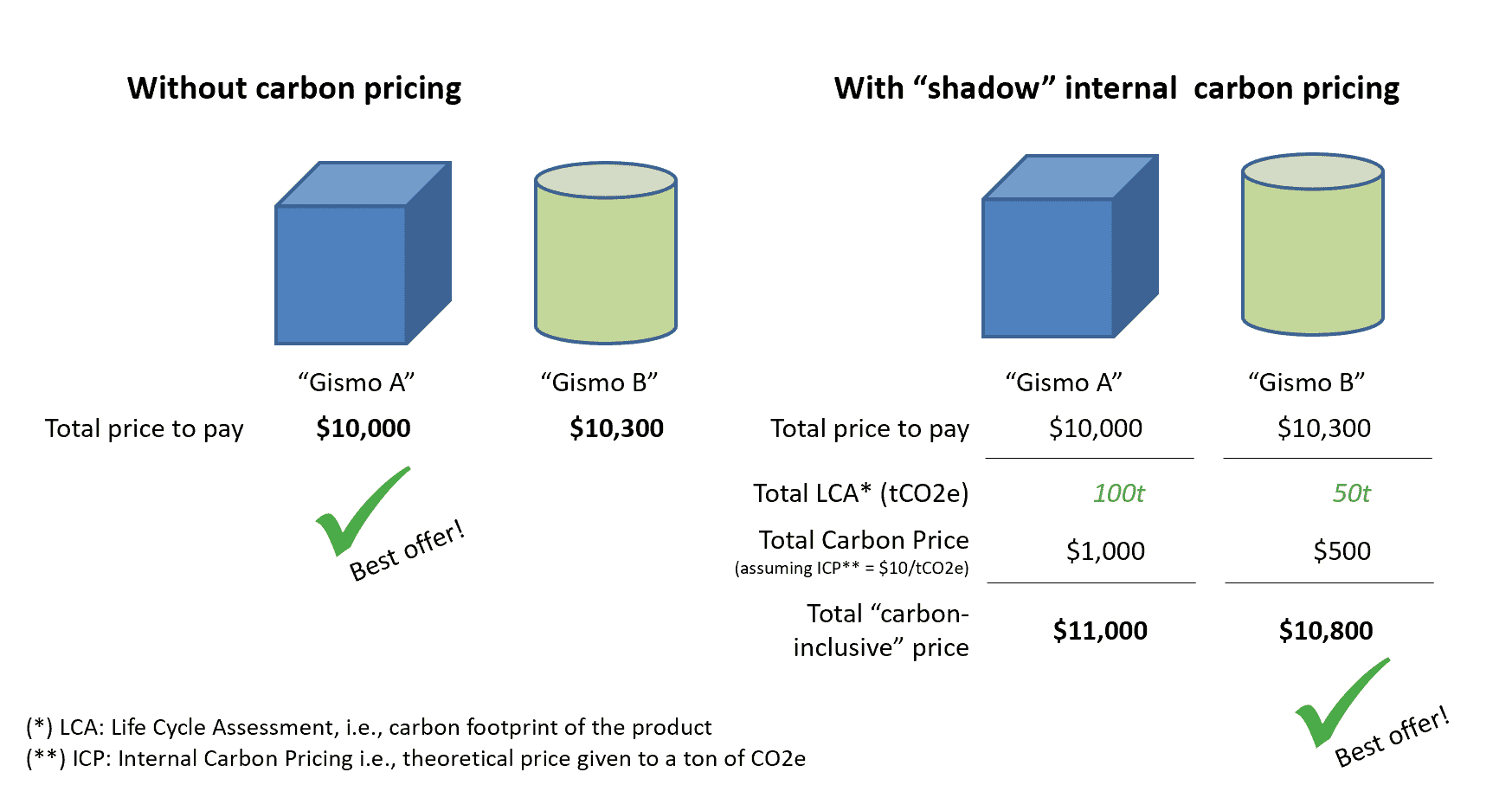

Shadow pricing mechanism: A hypothetical scenario applied to procurement

Scenario: Your purchasing department is tendering for the procurement of 1,000 much-needed “gismos”. The process is down to two potential suppliers that have met all the business requirements, including the latest CSR requirements:

Gismo A

Final offer = $10,000 for the lot

Gismo B

Final offer = $10,300 for the lot

In the above scenario, and without shadow pricing, Gismo A is most likely selected in the comfort that your purchasing department has integrated your sustainability policy into their qualitative set of selection criteria.

In our second scenario, your company has implemented shadow pricing for carbon. Let’s assume it has given a $10/tCO2e price. Your purchase department now requires suppliers to disclose the gismo’s Life Cycle Assessment or LCA determining the product’s overall carbon footprint.

Gismo A

Final offer = $10,000 for the lot

Total Carbon footprint of the offer (i.e., product LCA x1,000 units) = 100t CO2e

- Internal (shadow) pricing calculation = $10,000 + ($10 x 100t) = $11,000

Gismo B

Final offer = $10,300 for the lot

Total Carbon footprint of the offer (i.e. product LCA x1,000 units) = 50t CO2e

- Internal (shadow) pricing calculation = $10,300 + ($10 x 50t) = $10,800

Based on this scenario, and while the actual price to be paid to either supplier remains unchanged, given the $10/t price the company put on carbon, the procurement department will be inclined to select Gismo B, incidentally a more sustainable product that has a carbon footprint of half that of Gismo A…

—-

An internal trading system takes things to the next level by actually levying an internal tax on carbon within your organisation. Most companies, having opted for this would levy annually based on budget caps and credits systems (as opposed to a transactional approach) linked to their verified annual carbon reporting. This remains a much more complex system to implement which can be both punitive and rewarding. Its key advantage is in driving financial resources towards the area of the business contributing the most to your sustainability objectives and by extension, to the futureproofing of your business.

So, exactly how much is a ton of carbon?

There is no standard in this area, and anything goes to a certain extent! Examples range from anywhere between $2/t to over $200/t. What is important is first to understand the carbon intensity of your business, what you are looking to achieve, and how fast. The higher you set your price, the higher the expected impact. This can be good news for your sustainability performance, but perhaps quite disruptive to your short-term business results or overall competitiveness level.

To navigate through this balancing act and decide on the right level for you today, help might be on hand from different sustainability initiatives you may well already be part of. Science Based Targets (SBTi), the Carbon Disclosure Project (CDP) and the UN Global Compact (UNGC) all provide guidelines on the topic. If your organisation is expected to be directly impacted by future Carbon Taxation and de-risking is top of your agenda, then you may rather consider indexing your carbon price with the EU ETS or the California CCA. At the time this blog was edited, these were trading at just above EUR 85/t and USD 30/t respectively. If these levels seem like an unpalatable starting point, you can also look at aligning with other voluntary carbon markets (often industry-specific carbon offset markets). On the same date, some offset futures were trading at $2.50/t (Tech industry) or $5/t (Aviation industry).

If, by the end of this blog, you are now visualising a ton of carbon as this sombre, expensive, and – quite frankly – a bit scary-looking substance… we might just have made a small step in the right direction!

Supply Chain Enabled